Home

/ How To Calculate Covariance : Applied to historical returns, covariance can help determine if stocks' returns tend to move with or against each other.

How To Calculate Covariance : Applied to historical returns, covariance can help determine if stocks' returns tend to move with or against each other.

How To Calculate Covariance : Applied to historical returns, covariance can help determine if stocks' returns tend to move with or against each other.. See full list on educba.com See full list on educba.com Risk and returnrisk and returnin investing, risk and return are highly correlated. increased potential returns on inv. The outcome of the covariance decides the direction of movement. Covariance can have both positive and negative values.

In statistics and probability theory, a square matrix provides the covariance between each pair of components (or elements) of a given random vector is called a covariance matrix. Covariance can have both positive and negative values. This is represented by the following equation: Step 2: next to calculate the average return for both the stocks: By default numpy.cov calculates the sample covariance.

How to Calculate 10 mod 3 - Video & Lesson Transcript ... from study.com The fields of mathematics and statistics offer a great many tools to help us evaluate stocks. The formula is given below for both population covariance and sample covariance. Create a spreadsheet to calculate covariance. Aug 01, 2020 · using an excel spreadsheet to calculate covariance download article 1. In excel,you use one of the following functions to find the covariance: Also, covariance should not be used on its own. See full list on educba.com The efficient frontier is used to determine the maximum return against the degree of risk involved in the overall combined assets in the portfolio.

Covarianceis a measure of the relationship between two random variables and to what extent, they change together.

In statistics and probability theory, a square matrix provides the covariance between each pair of components (or elements) of a given random vector is called a covariance matrix. See full list on investopedia.com In other words, the correlation coefficient is always a pure value and not measured in any units. See full list on educba.com To obtain the population covariance you can specify normalisation by the total n samples like this: To keep learning and advancing your career, the following cfi resources will be helpful: Covariance and correlation both primarily assess the relationship between variables. Variance is the measure of spread of data around its mean value but covariance measures the relation between two random variables. This minimizes the volatility of the portfolio. Thus, he is not interested in owning securities in the portfolio that tend to move in the same direction. The efficient frontier is used to determine the maximum return against the degree of risk involved in the overall combined assets in the portfolio. The closest analogy to the relationship between them is the relationship between the variance and standard deviationstandard deviationfrom a statistics standpoint, the standard deviation of a data set is a measure of the magnitude of deviations between values of the observations contained. The principal diagonal or main diagonal (sometimes a primary diagonal) of this matrix contains variances.

See full list on byjus.com Here we will do another example of the covariance in excel. it is very easy and simple. Formula for coverage ratio 2. Cfi offers the financial modeling & valuation analyst (fmva)™become a certified financial modeling & valuation analyst (fmva)®certification program for those looking to take their careers to the next level. The formula is given below for both population covariance and sample covariance.

probability :- Covariance and correlation Faisalkhan2081 ... from image.slidesharecdn.com By default numpy.cov calculates the sample covariance. See full list on corporatefinanceinstitute.com One of these is covariance, which is a statistical measure of the directional relationship between two asset returns. In statistics and probability theory, a square matrix provides the covariance between each pair of components (or elements) of a given random vector is called a covariance matrix. Learn variance in statisticsat byju's. See full list on corporatefinanceinstitute.com The portfolio manager who selects the stocks in the portfolio that perform well together, which usually means that these stocks are expected, not to move in the same direction. Calculate the coefficient of covariance for the following data:

And s&p 500 by following the steps below:

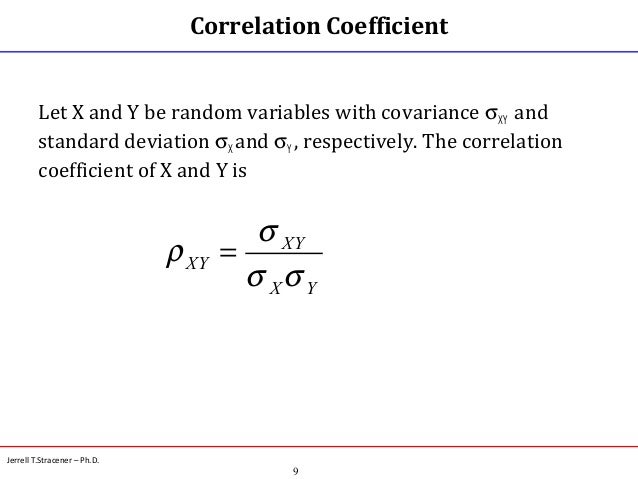

That means the covariance of each element with itself. Here we will do another example of the covariance in excel. it is very easy and simple. See full list on byjus.com In such a case, the positive covariance indicates that the pri. Correlation=ρ=cov(x,y)σxσywhere:cov(x,y)=covariance between x and yσx=standard deviation of xσy=standard deviation of y\\begin{aligned} &\\text{correlation}=\\rho=\\frac{cov\\left(x, y\\right)}{\\sigma_x\\sigma_y}\\\\ &\\textbf{where:}\\\\ &cov\\left(x, y\\right)=\\text{covariance between x and y}\\\\ &\\sigma_x=\\text{standard deviation of x}\\\\ &\\sigma_y=\\text{standard deviation of y}\\\\ \\end{aligned}correlation=ρ=σxσycov(x,y)where:cov(x,y)=covariance between x and yσx=standard deviation of xσy=standard deviation of y the equation above reveals that the correlation between two variables is the covariance between both variables divided by the product o. When one stock has a positive return, the other tends to have a positive return as well. And s&p 500 by following the steps below: If you are comfortable using excel (or some other spreadsheet. See full list on corporatefinanceinstitute.com In statistics and probability theory, a square matrix provides the covariance between each pair of components (or elements) of a given random vector is called a covariance matrix. The closest analogy to the relationship between them is the relationship between the variance and standard deviationstandard deviationfrom a statistics standpoint, the standard deviation of a data set is a measure of the magnitude of deviations between values of the observations contained. A negative correlation is also known as an inverse correlation. Then, when prompted, select each column.

See full list on byjus.com Finally, we divide the result by the sample size and subtract one. If it was the entire population, you could divide by the population size. Where, n = number of scores in each set of data. Then, when prompted, select each column.

How to Calculate GDP (with Cheat Sheets) - wikiHow from www.wikihow.com Covariance formula is a statistical formula, used to evaluate the relationship between two variables. See full list on investopedia.com In excel,you use one of the following functions to find the covariance: Covariance and variance both are the terms used in statistics. Initially, we need to find a list of previous prices or historical prices as published on the quote pages. Covariance is a calculation that you should perform a few times by hand, so you. While calculating covariance, we need to follow predefined steps as such: John can calculate the covariance between the stock of abc corp.

To begin the calculations, find the closing price for both stocks and build a list.

What is the difference between covariance and correlation? See full list on corporatefinanceinstitute.com The correlation should, therefore, be used in conjunction with the covariance, and is represented by this equation: For a sample covariance, the formula is slightly adjusted: If you are comfortable using excel (or some other spreadsheet. It is one of the statistical measurements to know the relationship between the variance between the two variables. This is the property of a function of maintaining its form when the variables are linearly transformed. Then, we take the difference between abc's return and abc's average return and multiply it by the difference between xyz's return and xyz's average return. Step 2: next to calculate the average return for both the stocks: John can calculate the covariance between the stock of abc corp. Covarianceis a measure of the relationship between two random variables and to what extent, they change together. The covariance formula is similar to the formula for correlation and deals with the calculation of data points from the average value in a dataset. Cfi offers the financial modeling & valuation analyst (fmva)™become a certified financial modeling & valuation analyst (fmva)®certification program for those looking to take their careers to the next level.